Part 1: Five SMART steps to take to help you sell more inventory, improve your inventory buying practices and increase profitability.

by David McMahon

Let’s simplify things. You make money by selling inventory. You lose money by buying inventory that does not sell and by incurring expenses associated with non-saleable inventory.

This article is about selling more inventory and improving inventory buying. I’m going to show you the core practices that the most profitable businesses follow to achieve the highest return on their inventory. We have built an acronym that defines these steps. It is called the 5 “SMART” Steps.

Learn to execute these 5 “SMART” Steps properly and you will significantly increase your profitability:

• Spot your best sellers.

• Maintain your winners.

• Auto identify and take action on DOGs.

• Reward high gross margin sales.

• Target market your customers in your database.

Step 1 - Spot Your Best Sellers

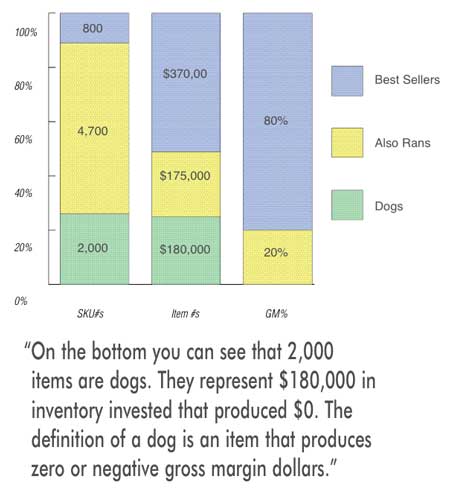

The chart below represents the blend of inventory SKUs (items) at an actual store. These numbers are typical for many retail furniture stores today. The blue shaded area represents best sellers or the winning items. The yellow shaded areas are the also-ran items or the lukewarm performing items. And the green shaded areas are unproductive inventory or the dogs. In this case, 800 items with a value of $370,000 at cost produced 80% of the gross margin dollars. This is the 80/20 principle in action. I guarantee that if we analyze your inventory, it will be similar to this. Most of your margin dollars will come from a minority of your items.

The chart also shows that 4,700 also-ran items had a value of $175,000 at cost and produced the remaining 20% of gross margin dollars. Also-rans are either best sellers that died out or dogs that finally sold.

On the bottom you can see that 2,000 items were dogs. They represented $180,000 in inventory invested that produced $0. The definition of a dog is an item that produces 0 or negative gross margin dollars.

This highlights the extreme importance of Step 1. Spot the best sellers. They are your gold. You need to know all of them, fast, and make sure that all managers and all employees know them as well. Without keeping tabs on these items you may never know the gold that you may have had. Here is how to spot these items:

• Each month, print a ranking of items underneath their respective categories and vendors ranked by gross margin volume produced for the prior 3 months. This keeps the analysis consistent and routine.

• Assign a 1, 2, or 3 ranking to the best selling items to represent the best of the best (#1), next of the best (#2), and rest of the best (#3). This establishes priority for you to follow (some systems can do this for you automatically).

• Post a top 100 item list in your lunch room.

• Have all managers educate the employees, especially salespeople, on where to find these items on the showroom floor and how to promote them to your customers. These items have the highest demand and produce the most profit. They are proven to be more “natural” to sell.

• If you are a custom order store where you sell in multi fabrics, identify your best sellers by the frame that produces highest margin dollars even though fabric can come in many combinations.

• Do it every month. Don’t stop.

Knowing and measuring is the first step to success. What is not measured cannot be improved. Do it with a system. No human can possibly keep track of the constantly changing dynamics of thousands of items. Those managers that continually focus on what works tend to produce greater results for the business. Those that operate using the seat-of-their pants mentality or who rely on a “recent memory system”, leave A LOT of dollars on the table.

Step 2: Maintain Your Winners!

It is tough to sell something if your customer can’t see it, right? That’s obvious. And if you agree with SMART Step 1 that best sellers produce the lion’s share of the profits and that knowing them is critical, then why do operations run out of these items?

The best performing businesses rarely run out of their best merchandise. These stores maintain their winners in stock at 95%. Thus their sales from these items are maximized. Average stores have their best sellers in stock about 85% of the time. Underperforming operations lose sales due to their lower percentage of in stock days.

Best seller “stock-outs” is the costliest of all inventory management issues. Suppose that you run out of an item that typically sells at just 2 pieces per month for an average margin of $750. If you run out of it for 2 months, what is your loss? $3,000 in margin. $6,000 in sales at 50% GM. And – less than happy salespeople, if they notice…

And that is just one item! Say that happens to 50 items per year. What then? That’s a $150,000 loss and $300,000 less in sales volume. You do not even see that on your Profit and Loss Statement.

To remedy the situation, minimize your loss and maximize your profits by using a system to track these factors on your winners:

• In stock and out of stock days.

• Sales – average units per month, actual units per 6 months and per year.

• Merchandising – displayed on floor? Nailed down on floor? Damaged?

• Lead time on average.

• Available quantity in stock to sell.

• Available quantity on order to sell and ETA date.

• GM, GMROI, ROI – gross margin produced and the return on investment of the item.

• Cost – raw cost, landed cost, and average cost.

• Current selling price and expected margin at that price point.

From this valuable item information you can then take these actions, to maintain your winners:

• See if you ran out of an item.

• Reorder the correct quantity.

• Display the item if not displayed.

• Nail down the item if it is a best seller (never sell the last best seller).

• Service damaged items and seek charge backs where required.

• Reorder at the right time and right quantity considering lead time and rate of sale.

• Fulfill a customer’s order sooner by seeing if there is sooner available merchandise.

• Do not over order, do not under order.

• See costing increases with respect to vendor and freight carrier.

• Check price point and margins at most recent costing – you will gain a huge amount of extra margin if you do this right.

Just in time inventory (JIT) supply without stock outs produces the highest returns. Maintain your winners and your profits will increase.

So what happens, if you order something and it dies out and becomes a dog like the rest of those profit moochers? See SMART Step 3 in the next issue of Furniture World…

David W. McMahon is an inventory management and operations expert. Questions about any aspect of retail operations management can be directed to David care of FURNITURE WORLD at davidm@furninfo.com or call him direct at 800-888-5564.